A financial crisis can feel like an insurmountable wall, especially when you are working with a limited income. However, having a structured response plan can be the difference between temporary hardship and long-term instability.

This guide provides a comprehensive roadmap designed to help low-income households navigate economic downturns. By focusing on liquidity, essential spending, and resource allocation, you can protect your family’s future.

Key Insights for Crisis Management

- Immediate Action: Assess your liquid assets and prioritize “Four Walls” spending (food, shelter, utilities, transport).

- Resource Utilization: Leverage local and federal assistance programs early rather than as a last resort.

- Debt Strategy: Focus on maintaining a minimum credit score while deferring non-essential payments.

- Sustainability: Small, consistent savings habits are more effective during a crisis than sporadic large contributions.

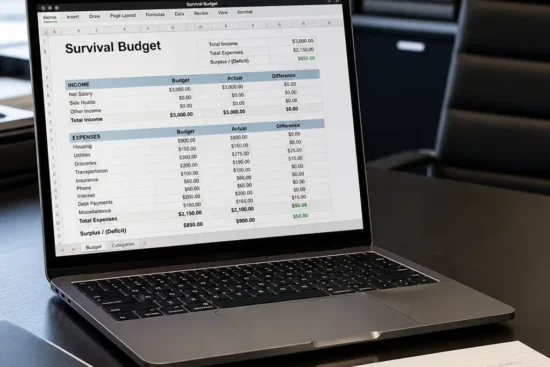

1. Immediate Crisis Assessment and Budgeting

When a financial crisis hits, the first step is a cold, hard look at the numbers. You cannot manage what you do not measure.

Start by listing every single source of income and every mandatory expense. For low-income families, this often reveals a “gap” that needs to be filled by either cutting costs or finding assistance.

The Zero-Based Budget Approach

In a crisis, every dollar must have a job. A zero-based budget ensures that your income minus your expenses equals zero at the end of the month.

- List Income: Include wages, side hustles, and government benefits.

- List Expenses: Start with the most critical survival needs.

- Calculate the Gap: If expenses exceed income, identify which “wants” can be eliminated immediately.

| Expense Category | Priority Level | Crisis Action |

|---|---|---|

| Housing/Rent | Critical | Negotiate payment plans early |

| Groceries | Critical | Use food banks to supplement |

| Utilities | High | Apply for LIHEAP assistance |

| Credit Cards | Low | Request a hardship forbearance |

2. Navigating the “Four Walls” of Finance

During a financial crisis, you must prioritize your “Four Walls.” These are the necessities required to keep your family safe and functioning.

Food and Nutrition

Don’t let pride stop you from using community resources. Organizations like Feeding America provide essential support for families facing food insecurity.

Shelter and Housing

If you cannot pay rent, communication is your best tool. Many landlords prefer a partial payment over a costly eviction process. Search for local rental assistance programs via your city’s official website.

Utilities and Basic Services

Many utility companies offer “Lifeline” programs or protection against shut-offs during extreme weather or documented financial hardship.

3. High-RPM Strategies: Debt vs. Savings

A common question during a financial crisis is whether to pay off debt or save cash. For low-income families, cash is king.

Comparison: Paying Debt vs. Building Liquidity

- Paying Debt: Reduces interest but leaves you vulnerable if an emergency occurs.

- Building Liquidity: Provides a safety net for immediate needs like car repairs or medical bills.

In most crisis scenarios, it is better to pay only the minimums on debt to keep as much cash on hand as possible. This ensures you don’t have to rely on high-interest payday loans which can trap you in a cycle of poverty.

4. Requirements and Eligibility for Assistance

Many families miss out on aid because they assume they don’t qualify. During a financial crisis, checking your eligibility is a high-priority task.

Common Assistance Programs

- SNAP (Supplemental Nutrition Assistance Program): Based on gross and net income limits.

- TANF (Temporary Assistance for Needy Families): Provides cash for basic needs.

- WIC: Specifically for pregnant women and children under five.

How to Apply

- Documentation: Gather pay stubs, social security cards, and utility bills.

- Application: Most states allow online applications through their Department of Human Services.

- Follow-up: Check your status weekly to ensure no additional paperwork is needed.

5. Generating Extra Income During a Crisis

While cutting expenses is vital, increasing income provides a more permanent solution to a financial crisis.

Low-Cost Online Income Ideas

- Micro-tasking: Using platforms like Amazon Mechanical Turk for small digital jobs.

- Online Tutoring: If you have expertise in a subject, digital classrooms are a great resource.

- Freelance Writing: Sharing your knowledge on finance or niche hobbies.

Cost Breakdown of Starting a Side Hustle

| Startup Cost | Potential Monthly Income | Difficulty Level |

|---|---|---|

| $0 (Freelancing) | $200 – $1,000 | Moderate |

| $20 (Reselling) | $100 – $500 | Easy |

| $0 (Surveys) | $20 – $50 | Very Easy |

6. Protecting Your Credit Score

A financial crisis often damages your credit, making it harder to recover later. You can mitigate this by being proactive with lenders.

Ask for a “Hardship Program.” Many banks will lower your interest rate or allow you to skip a payment without reporting it as “late” to the credit bureaus. This protects your long-term financial health and ensures you can access lower rates when the crisis ends.

7. Pros and Cons of Common Survival Tactics

| Strategy | Pros | Cons |

|---|---|---|

| Credit Card Usage | Immediate liquidity | High interest rates later |

| Borrowing from Family | Usually 0% interest | Can strain relationships |

| Selling Assets | Fast cash injection | Only a one-time solution |

| Reducing Insurance | Lowers monthly bills | Risk of massive future costs |

8. Building a Post-Crisis Buffer

Once the immediate financial crisis subsides, the goal shifts to prevention. This involves building a “Starter Emergency Fund.”

For low-income families, aiming for $1,000 is a great first milestone. This amount covers most minor car repairs or a small medical deductible, preventing you from slipping back into debt.

Steps to Maintain Stability

- Automate Savings: Even $5 a week adds up over a year.

- Review Insurance: Ensure you have basic coverage to prevent a total loss.

- Continuous Learning: Improve your skills to increase your earning potential over time.

Conclusion and Action Plan

Navigating a financial crisis requires a blend of discipline, resourcefulness, and proactive planning. By prioritizing your Four Walls and utilizing community assistance, you can weather the storm without losing your long-term stability.

Remember, a low income does not mean you are powerless. Start by tracking your spending today and reach out to one assistance program this week.

What is your biggest challenge in saving during a crisis? Share your thoughts in the comments below or share this article with someone who needs a plan.

Take the first step toward security by creating your crisis budget now. For more tips on resilient living, visit our guide on saving for beginners.

Leave a Reply