Reaching your target retirement age earlier than expected is an incredible financial milestone. It is the ultimate payoff for years of disciplined saving, smart investing, and strategic lifestyle choices.

However, stepping away from the workforce early introduces a unique set of structural financial challenges. You must manage your wealth over a significantly longer horizon without the safety net of immediate state benefits.

When you transition to this new phase, your primary objective shifts from wealth accumulation to strategic wealth preservation. This transition requires a fundamental restructuring of your monthly cash flow.

Navigating the gap between your early retirement date and the age when you can access government benefits requires a specialized budgeting framework. This guide details how to build and maintain that framework.

Key Insights / Quick Summary

For quick reference, here is a breakdown of the critical adjustments required when you transition to early retirement:

| Financial Element | Standard Timeline | Early Retirement Adjustment | Core Strategy |

|---|---|---|---|

| Medicare Eligibility | Age 65 | Private insurance coverage required | ACA Marketplace plans with tax subsidies |

| Penalty-Free Withdrawals | Age 59½ | Roth Ladder or Rule 72(t) | Tax-advantaged conversion and distribution |

| Social Security | Age 62 to 70 | Delaying benefits increases payouts | Live on taxable brokerage assets first |

| Safe Withdrawal Rate | Traditional 4% Rule | Reduce to 3.0% – 3.5% | Protects against prolonged market downturns |

The Reality of Reaching Your Retirement Age Early

The traditional definition of retirement age is shifting rapidly as more people seek financial independence. For generations, retirement planning revolved around reaching age 65, the gateway to Medicare and full retirement benefits.

When you achieve early retirement, you are essentially buying back your time. This means your investment portfolio must sustain your lifestyle for potentially 30, 40, or even 50 years.

This prolonged timeline changes how you view asset allocation, inflation, and spending flexibility. Traditional rules of thumb that work for a 65-year-old may lead to premature portfolio depletion for an early retiree.

[ Early Retirement Date ] ──► (The Gap Years) ──► [ Standard Retirement Age ]

│ │

• Private Healthcare • Medicare (Age 65)

• Roth Conversion Ladders • Standard Withdrawals

• Taxable Brokerage Assets • Social Security

To safeguard your nest egg, you must establish clear mechanisms to bridge the gap before you hit the traditional retirement age set by government programs. This requires optimizing tax brackets, securing affordable healthcare, and avoiding early withdrawal penalties.

Bridging the Healthcare Gap

One of the largest hurdles for early retirees is securing high-quality health insurance. Before reaching your traditional retirement age, employer-sponsored healthcare plans are no longer an option.

Medicare does not begin until you reach age 65. If you retire at age 50 or 55, you face a decade or more of navigating private insurance markets.

Failing to budget accurately for healthcare is one of the most common reasons early retirements fail. Even a minor medical emergency can derail an unstructured budget if you lack proper coverage.

Avoiding Early Withdrawal Penalties

Many retirement savers keep their wealth in traditional 401(k) plans or Traditional IRAs. However, the IRS generally imposes a 10% penalty on distributions taken before age 59½.

This means your money might be locked away right when you need it most. Accessing your capital without triggering penalties requires proactive, multi-year planning.

To avoid these costly penalties, you must understand how to tap your retirement accounts early through specialized strategies. Understanding these rules ensures your money remains accessible throughout your transition.

Designing Your Early Retirement Budget: Step-by-Step

Creating a sustainable budget for early retirement is not about deprivation; it is about absolute cash flow clarity. You must design a system that dynamically adapts to market conditions.

Here is a step-by-step process to build a robust financial framework that scales with your lifestyle.

Step 1: Audit and Categorize Fixed vs. Variable Costs

Begin by categorizing your current and future expenses into two distinct buckets: non-discretionary (essential) and discretionary (lifestyle) spending.

- Non-Discretionary Expenses: Housing, basic groceries, health insurance premiums, property taxes, utilities, and essential transport.

- Discretionary Expenses: Travel, dining out, hobbies, subscription services, and luxury purchases.

This distinction is vital. If the financial markets experience a downturn, your discretionary spending is the first lever you will pull to protect your portfolio.

Having a clear understanding of your bare-minimum living costs gives you immense control over your withdrawal rate. It provides psychological comfort when market volatility arises.

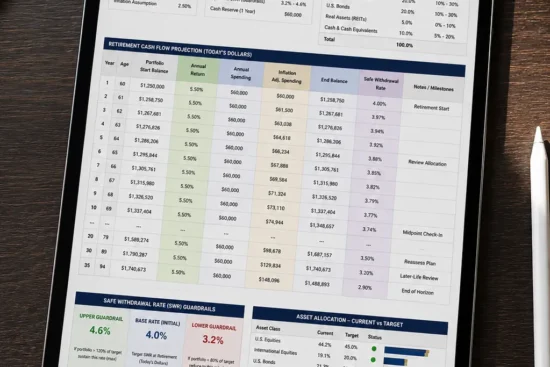

Step 2: Establish Your Safe Withdrawal Rate (SWR)

The classic “4% rule” suggests you can withdraw 4% of your portfolio in year one of retirement and adjust that amount for inflation annually. However, this rule was modeled for a traditional 30-year retirement horizon.

If you reach your retirement age early, your retirement could easily span 40 to 50 years. Over this timeframe, a 4% withdrawal rate carries a significantly higher risk of portfolio exhaustion.

┌─────────────────────────────────────────────────────────────┐

│ SAFE WITHDRAWAL RATE GUIDE FOR RETIREES │

├──────────────────────────────┬──────────────────────────────┤

│ Retirement Duration │ Recommended Safe Rate │

├──────────────────────────────┼──────────────────────────────┤

│ 25-30 Years │ 3.75% - 4.0% │

│ 35-40 Years │ 3.25% - 3.5% │

│ 45+ Years │ 3.00% - 3.25% │

└──────────────────────────────┴──────────────────────────────┘

Many financial planners recommend reducing your safe withdrawal rate to 3.0% or 3.5% for early retirement. This conservative adjustment accounts for prolonged market cycles and the eroding effects of long-term inflation.

Step 3: Account for Inflation and Market Downturns

Inflation is the silent destroyer of purchasing power. Over a 40-year early retirement, even a moderate 2.5% annual inflation rate will more than double the cost of your basic living expenses.

Your budget must assume that your nominal expenses will rise every single year. This means your portfolio must remain positioned for long-term growth, even while you are actively withdrawing from it.

Furthermore, you must prepare for “Sequence of Returns Risk.” This is the risk that a market crash occurs early in your retirement, forcing you to sell depreciated assets and permanently reducing your portfolio’s recovery potential.

To mitigate this risk, you can adopt a dynamic spending strategy. This involves reducing your discretionary spending by a predetermined percentage during down market years.

Step 4: Build a Cash Cushion (The Buffer Strategy)

To avoid selling stocks during a market downturn, you should maintain a robust cash or short-term cash equivalent cushion. This cash buffer should ideally cover 1 to 3 years of living expenses.

Keep these funds in high-yield savings accounts, short-term treasury bills, or money market funds. This asset class maintains principal stability while still generating yield.

When the market experiences a correction, you stop withdrawing from your equity portfolio entirely. Instead, you live off your cash buffer until the market recovers, protecting your core investment shares.

Strategic Income Mapping Before Traditional Retirement Age

Accessing your retirement savings before reaching standard retirement age requires utilizing specific, tax-compliant strategies. The goal is to maximize your tax efficiency while avoiding IRS penalties.

There are three primary vehicles early retirees use to construct their income streams.

┌────────────────────────────────────────┐

│ EARLY RETIREMENT INCOME STREAMS │

└───────────────────┬────────────────────┘

│

┌────────────────────────────┼────────────────────────────┐

▼ ▼ ▼

[ Taxable Brokerage ] [ Roth IRA Ladder ] [ Rule 72(t) / SEPP ]

• High accessibility • 5-year waiting period • Rigid annual payments

• Capital gains rates • Tax-free distributions • No penalty on IRA

The Roth IRA Conversion Ladder

The Roth IRA conversion ladder is a highly effective tool for early retirees. This strategy allows you to convert pre-tax Traditional IRA or 401(k) funds into a Roth IRA, making them accessible penalty-free.

To execute this, you convert a portion of your traditional assets to a Roth IRA each year. You pay income tax on the converted amount in the year of the conversion.

Five years after each conversion, those specific funds can be withdrawn completely penalty-free and tax-free. By setting up consecutive annual conversions, you create a steady stream of tax-free income five years down the road.

To read up on the official tax treatment of these moves, consult the IRS early distribution rules before initiating any conversions.

Rule 72(t) / Substantially Equal Periodic Payments (SEPP)

If you have a traditional IRA and need immediate income without waiting five years, the IRS allows you to use Rule 72(t). This rule permits penalty-free early withdrawals via Substantially Equal Periodic Payments (SEPP).

Under this rule, you must take annual distributions based on life expectancy calculations provided by the IRS. These payments must continue for at least five years or until you reach age 59½, whichever is longer.

The primary disadvantage of SEPP is its rigidity. If you modify or stop the payments early, the IRS retroactively applies the 10% penalty to all prior distributions.

Because of this lack of flexibility, Rule 72(t) should only be used if you have a highly stable, predictable base of expenses that aligns with the calculated distribution amounts.

Utilizing Taxable Brokerage Accounts First

Using a standard, taxable brokerage account is the most straightforward way to fund the years before you reach retirement age. Taxable accounts carry no age-based withdrawal restrictions or early withdrawal penalties.

Furthermore, long-term capital gains tax rates are significantly lower than ordinary income tax rates. For many early retirees with modest living expenses, the federal tax rate on long-term capital gains can be as low as 0%.

Selling appreciated assets in a taxable account allows you to fund your lifestyle with minimal tax friction. This preserves your tax-advantaged retirement accounts, allowing them to compound uninterrupted for decades.

Healthcare Options for Early Retirees

Securing high-quality health insurance is critical to protecting your early retirement nest egg. Without an employer-sponsored plan, you must navigate your healthcare options proactively.

The following options are the most viable paths for early retirees.

Leveraging the Affordable Care Act (ACA) Subsidies

The Health Insurance Marketplace established under the Affordable Care Act (ACA) is a powerful tool for early retirees. ACA plan premiums are heavily subsidized based on your Modified Adjusted Gross Income (MAGI).

Because your early retirement income comes from investment withdrawals rather than salary, you have significant control over your declared income. By keeping your taxable income low, you can qualify for substantial premium tax credits.

To maximize these subsidies, you must coordinate your taxable distributions carefully. For details on enrolling, you can search for plan options directly on the official Health Insurance Marketplace options page.

Maxing Out Health Savings Accounts (HSAs)

If you have access to a High-Deductible Health Plan (HDHP) during your working years, you should maximize your Health Savings Account (HSA) contributions. HSAs offer a unique triple tax advantage:

- Contributions are 100% tax-deductible.

- The account balance grows entirely tax-free.

- Withdrawals are completely tax-free when used for qualified medical expenses.

Once you reach age 65, your HSA functions similarly to a traditional IRA. You can withdraw funds for any non-medical expense and pay only standard income tax, with no penalties.

Using an HSA to pay for healthcare expenses during early retirement protects your other investment portfolios. It acts as a dedicated, tax-exempt bucket for your medical needs.

Pros and Cons of Early Retirement Budgeting

Transitioning your budget before reaching standard retirement age involves distinct structural trade-offs.

Pros:

- Total Time Freedom: You gain complete control over your daily schedule during your healthiest, most active years.

- Tax Optimization Control: With no active salary, you can precisely control your tax bracket by managing your asset withdrawals.

- Lifestyle Design: Early retirement allows you to transition into consulting, passion projects, or slow travel on your own terms.

- Generational Impact: Modeling smart wealth preservation early can pass down healthy financial habits to your family.

Cons:

- Extended Portfolio Lifespan: Your assets must support you for a much longer period, increasing the impact of inflation and market risk.

- Complex Withdrawal Rules: Navigating Roth conversion ladders, SEPP, and IRS penalty exemptions requires meticulous annual record-keeping.

- High Health Insurance Costs: You must pay out-of-pocket for health insurance premiums for years before becoming eligible for Medicare.

- Reduced Social Security Payouts: Claiming retirement benefits before your full retirement age permanent reduces your monthly payout.

Common Early Retirement Budgeting Mistakes

Even experienced investors make critical errors when managing their money in early retirement. Avoiding these common traps is vital to securing your long-term financial independence.

1. Underestimating Future Tax Rates

Many early retirees assume their tax rates will remain low forever. However, once you reach age 73, you must start taking Required Minimum Distributions (RMDs) from traditional pre-tax accounts.

These mandatory distributions can easily push you into a much higher tax bracket later in life. This highlight the importance of performing strategic Roth conversions during your lower-income early retirement years.

2. Failing to Prepare for Sequence of Returns Risk

Withdrawing too aggressively during the first few years of early retirement can permanently damage your portfolio. If the market experiences a prolonged downturn during this initial phase, your portfolio may never fully recover.

Always maintain a cash reserve and prepare to reduce your discretionary spending during market downturns. This flexibility is the ultimate defense against sequence of returns risk.

3. Claiming Social Security Too Early

While you can claim Social Security as early as age 62, doing so permanently reduces your monthly benefit. For every year you delay benefits past your full retirement age up to age 70, your benefit increases by roughly 8% annually.

To see how early claims affect your long-term payout numbers, consult the Social Security Administration’s early retirement rules to run a personalized calculation.

Expert Insights on Wealth Preservation

We reached out to certified financial planners specializing in early retirement to share their top strategies for maintaining a sustainable retirement runway.

“The biggest mistake early retirees make is viewing their budget as static. A successful early retirement budget must function like a thermostat, not a thermometer. It must actively adjust your spending based on the performance of your portfolio.”

— David Vance, CFP®, Wealth Management Specialist

Additionally, automated portfolio rebalancing is a critical tool. Rebalancing ensures that your asset allocation stays aligned with your risk tolerance, preventing your portfolio from becoming overly concentrated in volatile assets.

Frequently Asked Questions

What is the safest withdrawal rate for a 40-year early retirement?

For a retirement lasting 40 years or more, a withdrawal rate of 3.0% to 3.5% is generally considered safe. This conservative rate protects your portfolio against prolonged market downturns and the compounding effects of long-term inflation.

Can I withdraw money from my 401(k) at age 55 without penalty?

Yes, under the IRS “Rule of 55.” If you leave or lose your job in or after the calendar year you turn 55, you can withdraw funds from that specific employer’s 401(k) plan penalty-free. This rule does not apply to prior employers’ plans or Traditional IRAs.

How do I manage health insurance if I retire at age 50?

Before reaching standard retirement age, your best health insurance option is typically the ACA Health Insurance Marketplace. By carefully managing your taxable distributions, you can keep your MAGI low and qualify for substantial premium tax credits.

Should I pay off my mortgage before retiring early?

Paying off your mortgage eliminates your largest monthly fixed expense, significantly reducing your baseline lifestyle cost. This lower monthly requirement lowers your required safe withdrawal rate, reducing overall portfolio risk.

How does early retirement affect my Social Security benefits?

Reaching retirement age early means you will have fewer high-earning years included in your Social Security calculation. Since benefits are based on your highest 35 years of inflation-adjusted earnings, years with $0 income will lower your eventual monthly payout.

What is a Roth IRA conversion ladder?

A Roth IRA conversion ladder is a strategy used to access pre-tax retirement funds penalty-free before age 59½. By converting Traditional IRA funds to a Roth IRA annually, you can withdraw those specific converted amounts tax-free and penalty-free after a five-year waiting period.

Conclusion

Reaching your target retirement age early is a life-changing accomplishment. However, transitioning from wealth accumulation to long-term wealth preservation requires a highly disciplined, adaptable budgeting strategy.

By establishing a conservative safe withdrawal rate, building a robust cash buffer, optimizing your healthcare options, and utilizing tax-efficient withdrawal strategies, you can secure your financial freedom for decades to come.

Take control of your retirement runway today. Begin by auditing your fixed versus variable expenses, and outline a multi-year income map that minimizes taxes and maximizes peace of mind.

Leave a Reply